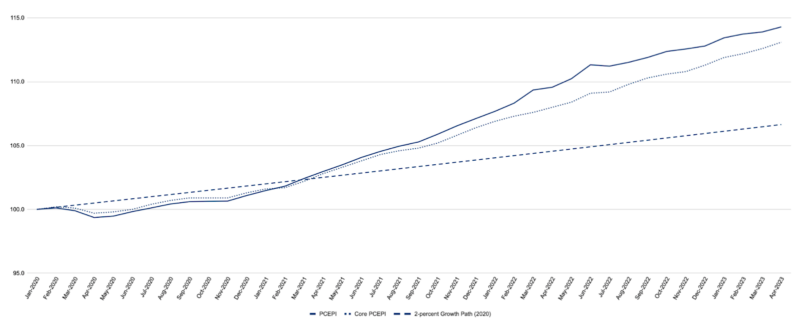

The latest inflation data is not what Federal Reserve officials were hoping for. The Personal Consumption Expenditures Price Index (PCEPI), which is the Fed’s preferred measure of inflation, grew at a continuously-compounding annual rate of 4.2 percent from April 2022 to April 2023, up from 4.1 percent for the twelve-month period ending in March 2023. The PCEPI has grown 4.1 percent per year since January 2020, just prior to the pandemic. Prices today are 7.7 percentage points higher than they would have been had the Fed hit its 2 percent target over the period.

Core inflation, which excludes volatile food and energy prices and is thought to be a better predictor of future inflation, also remained high. Core PCEPI grew 4.6 percent from April 2022 to April 2023, up from 4.5 percent for the twelve-month period ending in March 2023. Core PCEPI has grown 3.8 percent per year since January 2020, and is now 6.5 percentage points above the target growth path expected prior to the pandemic.

Fed officials may worry that the disinflation process has stalled. For this reason, the latest data likely increases uncertainty about the future course of monetary policy.

The Federal Open Market Committee raised its federal funds rate target range to 5.0 – 5.25 percent earlier this month, the tenth hike in fifteen months, but signaled it might pause rate hikes in June. Back in March, the FOMC had said it anticipated “that some additional policy firming may be appropriate.” It’s statement was revised at the May meeting, when the FOMC said it would “take into account the cumulative tightening of monetary policy, the lags with which monetary policy affects economic activity and inflation, and economic and financial developments” in order to determine “the extent to which additional policy firming may be appropriate to return inflation to 2 percent over time.”

In the time since the last meeting, FOMC members have expressed conflicting views.

Some FOMC members, including Chair Powell, continue to suggest a pause may be in order. “Until very recently,” Powell told attendees at a recent Fed conference, “it has been clear that further policy firming would be required. As policy has become more restrictive, the risks of doing too much versus doing too little are becoming more balanced—and our policy has adjusted to reflect that fact. We haven’t made any decisions about the extent to which additional policy firming would be appropriate, but given how far we’ve come […] we can afford to look at the data and the evolving outlook and make careful assessments.”

Governor Philip Jefferson has similarly suggested that a pause may be appropriate. “History shows that monetary policy works with long and variable lags, and that a year is not a long enough period for demand to feel the full effect of higher interest rates. Another factor weighing on my thinking is the uncertainty about tighter lending standards that I mentioned earlier.”

Other FOMC members have hinted at cutting rates in the not-so-distant future. “You don’t land the plane nose down,” Chicago Fed President Austan Goolsbee told New York Times columnist Jeana Smialek earlier this month. “When you come in for the landing, you’ve got to soften the blow a little.”

Still others suggest the FOMC has not gone far enough. Minneapolis Fed President Neel Kashkari has indicated he “would rather err on being a little bit more hawkish rather than regretting it and having been too dovish” because the cost of not getting inflation down to 2 percent is much higher to Main Street than the cost of getting it down to 2 percent.”

Dallas Fed President Lorie Logan left open the possibility for a pause, but also suggested rates would likely need to go higher. “The data in coming weeks could yet show that it is appropriate to skip a meeting,” she said, “though, we aren’t there yet.”

Governor Waller has expressed a similar skip-then-raise view. “If one is sufficiently worried about this downside risk, then prudent risk management would suggest skipping a hike at the June meeting but leaning toward hiking in July based on the incoming inflation data,” he said.

The latest inflation data is unlikely to alleviate the concerns of Kashkari, Logan, and Waller. But how much has it moved the needle, particularly among those FOMC members who previously appeared to be more committed to a pause? With one vacancy, it currently takes six votes to pass a decision.

The CME Group suggests the needle has moved considerably. It currently puts the odds of a June rate hike at 53.9 percent, up from just 17.4 percent one week ago.

THIS ARTICLE ORIGINALLY POSTED HERE.

– David Skarica")