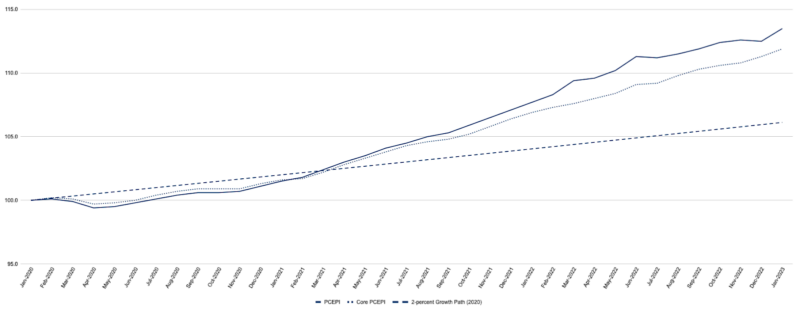

After eight rate hikes from the Federal Reserve in the last year and declining inflation during the back half of 2022, many had hoped the worst of the price increases were behind us. Today’s release from the Bureau of Economic Analysis suggests that might not be the case. The personal consumption expenditures price index (PCEPI), which is the Fed’s preferred measure of inflation, grew at an annualized rate of 7.4 percent in January 2023 — the highest one-month posting since June 2022.

The PCEPI has grown at a continuously compounding annual rate of 4.2 percent since January 2020, just prior to the pandemic. As a consequence, prices are 7.4 percentage points higher today than they would have been had the Fed hit its 2-percent target over the period.

Core PCEPI inflation, which excludes volatile food and energy prices and is widely thought to be a better predictor of future inflation, also climbed over the last few months. In November 2022, core PCEPI grew at an annualized rate of just 2.6 percent. It ticked up to 4.5 percent in December 2022, followed by an incredibly steamy 6.8 percent in January 2023.

The recent surge in inflation means monetary policy has not been as restrictive as Fed officials had intended. The Federal Open Market Committee (FOMC) raised its (nominal) federal funds rate target range to 4.5 to 4.75 on February 1. If inflation expectations were equal to the previous month’s core PCEPI inflation rate, the current nominal target range would imply a real (inflation-adjusted) federal funds rate range of -2.0 to -1.75 percent — well below 0.25 percent, which many economists cite as an estimate of the neutral rate.

Had Fed officials known inflation was surging in January, they may have opted for a larger rate hike at their last meeting. Indeed, the FOMC meeting minutes — released on Wednesday — indicate that a few participants “favored raising the target range for the federal funds rate 50 basis points” at the previous meeting or “could have supported raising the target by that amount.” Cleveland Fed president Lorretta Mester and St. Louis Fed president James Bullard were among those pushing for higher rates. Neither Mester nor Bullard currently vote on the FOMC, but they do participate in the policy discussion.

Whether the FOMC will continue to raise rates in 25-basis-point increments or opt for a bigger hike in March remains to be seen. Most FOMC members have said they prefer making smaller moves at this point. But they did not expect such a large inflation reading. And they surprised markets last June by opting for a 75-basis-point hike, after Chair Jerome Powell had said rate hikes in excess of 50 basis points were off the table at the post-meeting press conference in May.

While the size of the coming rate hikes is uncertain, there is somewhat more certainty about where rates are ultimately going: higher.

In December, the Federal Open Market Committee projected just three 25-basis-point rate hikes in 2023. That would have taken the federal funds rate target range to 5.0 to 5.25 percent. Now, the CME Group reports a 55.4 percent chance that the federal funds rate target range will be 5.25 to 5.5 percent, following the June 2023 meeting, and a 31.3 percent chance the range will be 25 basis points higher than that in July. The FOMC will revise its projections in March.

How high rates will ultimately go depends on how inflation evolves over the next few months — and how quickly the Fed reacts to restore confidence in its longer term-inflation projections. The January PCEPI release marked a step in the wrong direction.

THIS ARTICLE ORIGINALLY POSTED HERE.

– David Skarica")