Has the Discount Window Mystery been Solved?

On January 25th, I wrote about the increasing borrowing activity taking place at the Fed’s discount window. I commented that, despite popular perceptions, not all the borrowing at the discount window is driven by emergencies. But I also added that with rapidly rising interest rates, and the money supply contracting for the first time in decades and possibly the quickest that it ever has, the beginning of a liquidity crisis was nevertheless a distinct possibility.

I wrote then:

Nothing is conclusive yet. In about 18 months, the identity of the firms which have been tapping the Fed’s discount window starting in March 2022 will become publicly available. If those funding requests simply stem from navigating the ongoing effects of the economic maelstrom of 2022, we’ll learn at that time. If something worse is brewing, much sooner.

It is not yet known whether Silicon Valley Bank (SVB) was the firm, or one of several, borrowing at the discount window. There are several things we do know, however. First, the SVB collapse is the second-largest bank failure in US history. Second, that the bank had been desperately trying to sell assets and lost a few billion dollars doing so. And third, as of late December, SBV held 57 percent of its total assets in investments while the average among 74 similar competitors was about 42 percent. Of those investments, $108 billion were in US Treasury and agency securities — an asset class which had its worst year on record in 2022.

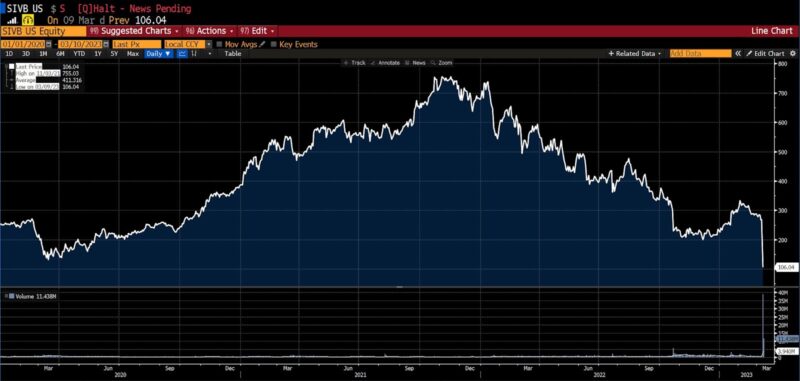

In November 2021, the stock hit an all time high of $755 per share, then joined the rest of the market in the 2022 price declines. March has proven brutal. After drifting sideways between about $250 and $350 since the start of 2023, the stock price fell from $283 on Monday, March 6, to hover in the $267 range on March 8 and 9, and then collapsed to $106.04 on Thursday March 9. At just before 9am this morning, March 10, trading was halted.

Silicon Valley Bank (2020 – present)

Federal Depository Insurance Company (FDIC) filings indicate that US banks took over $600 billion worth of unrealized losses last year, a large portion of which was generated by precipitously falling bond prices amid the Fed’s aggressive interest rate hikes. In addition to holding $108 billion in Treasuries during the worst year in history for such securities, SVB’s books include $74 billion in loans, a portion of which were undoubtedly extended to local tech companies. Tech companies have recently been under pressure as well, and are cutting costs.

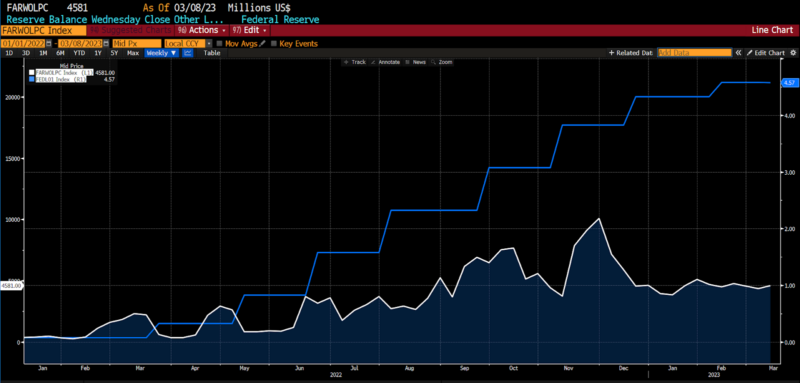

Fed Discount Window activity vs. Effective Fed Funds rate (2020 – present)

Since the end of 2019, Federal Reserve policies have pumped up the monetary base by trillions of dollars. As kids today say, “Money printer [went] brr.” The reversal of that process and the tightening of financial conditions has driven annualized M2 growth negative for the first time on record. Whereas, until recently, contractionary policies were broadly impacting the profitability of interest-rate-sensitive firms, for some it is now threatening their survival.

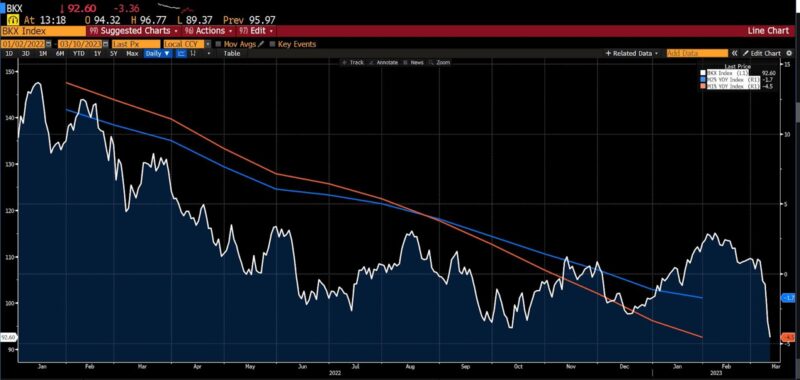

KBW Bank Index (white) vs. annualized growth in M1 (orange) and M2 (blue) monetary aggregates (2022 – present)

The value of loans taken when rates were low have plunged, and depositors are expecting higher rates. Financial institutions and firms which borrowed from them amid two decades at lower-than-normal rates are already experiencing the effects of simple normalization. The combination of the SVB development on top of yesterday’s disclosure by Silvergate Capital Corp that it would cease operation amid the wreckage of the cryptocurrency industry, couldn’t come at a much worse time. Estimates for the Fed’s terminal policy rate are creeping toward 6 percent amid persistent inflation in services and too-strong-for-comfort employment data. If history and market-implied policy rates are any guide, it won’t take much more pain in the financial sector for the Fed to begin easing rates again.

We won’t know for another twelve or fourteen months whether Silicon Valley Bank (or any of the other banks being thrown overboard today) were the ones borrowing at the Fed’s discount window. But it is increasingly likely that whatever firm(s) it was, exigency was the driver.

THIS ARTICLE ORIGINALLY POSTED HERE.

– David Skarica")