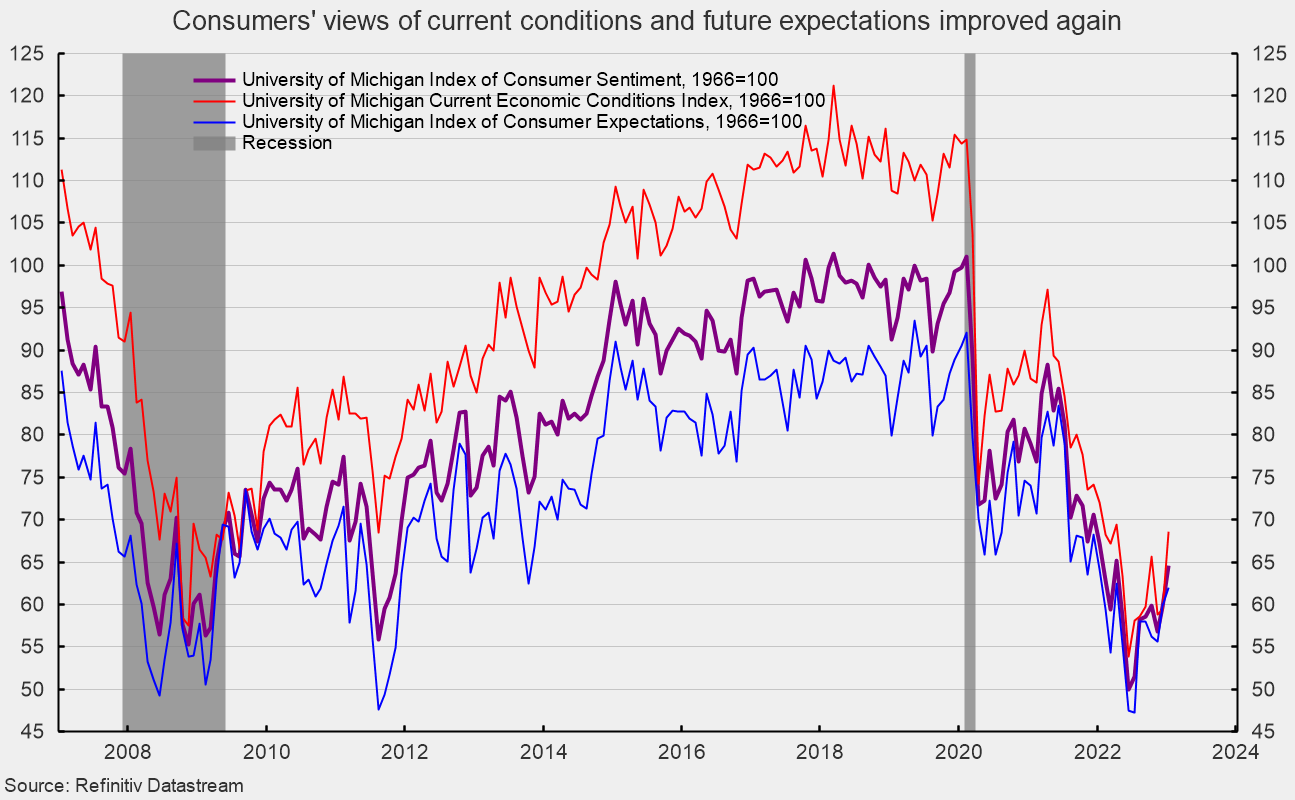

The preliminary January results from the University of Michigan Surveys of Consumers show overall consumer sentiment improved for the month but remains low (see first chart). The composite consumer sentiment index increased to 64.6 in January, up from 59.7 in December. The index hit a record low of 50.0 in June and is down from 101.0 in February 2020 at the onset of the lockdown recession. The increase in January totaled 4.9 points or 8.2 percent. The level of the composite index remains consistent with prior recessions, but the solid improvement from the 2022 low is a positive sign.

The current-economic-conditions index rose to 68.6 versus 59.4 in December (see first chart). That is a 9.2-point or 15.5 percent increase for the month. This component is 14.8 points above the June low of 53.8 and is at the highest level since April.

The second component — consumer expectations, one of the AIER leading indicators — gained 2.1 points, or 3.5 percent for the month, to 62.0. This component index is 14.7 points above the July 2022 low of 47.3 and is at the highest level since April (see first chart).

According to the report, “Consumer sentiment remained low from a historical perspective but continued lifting for the second consecutive month, rising 8% above December and reaching about 4% below a year ago.” The report adds, “Current assessments of personal finances surged 16% to its highest reading in eight months on the basis of higher incomes and easing inflation. Although the short-run economic outlook fell modestly from December, the long-run outlook rose 7% to its highest level in nine months and is now 17% below its historical average.”

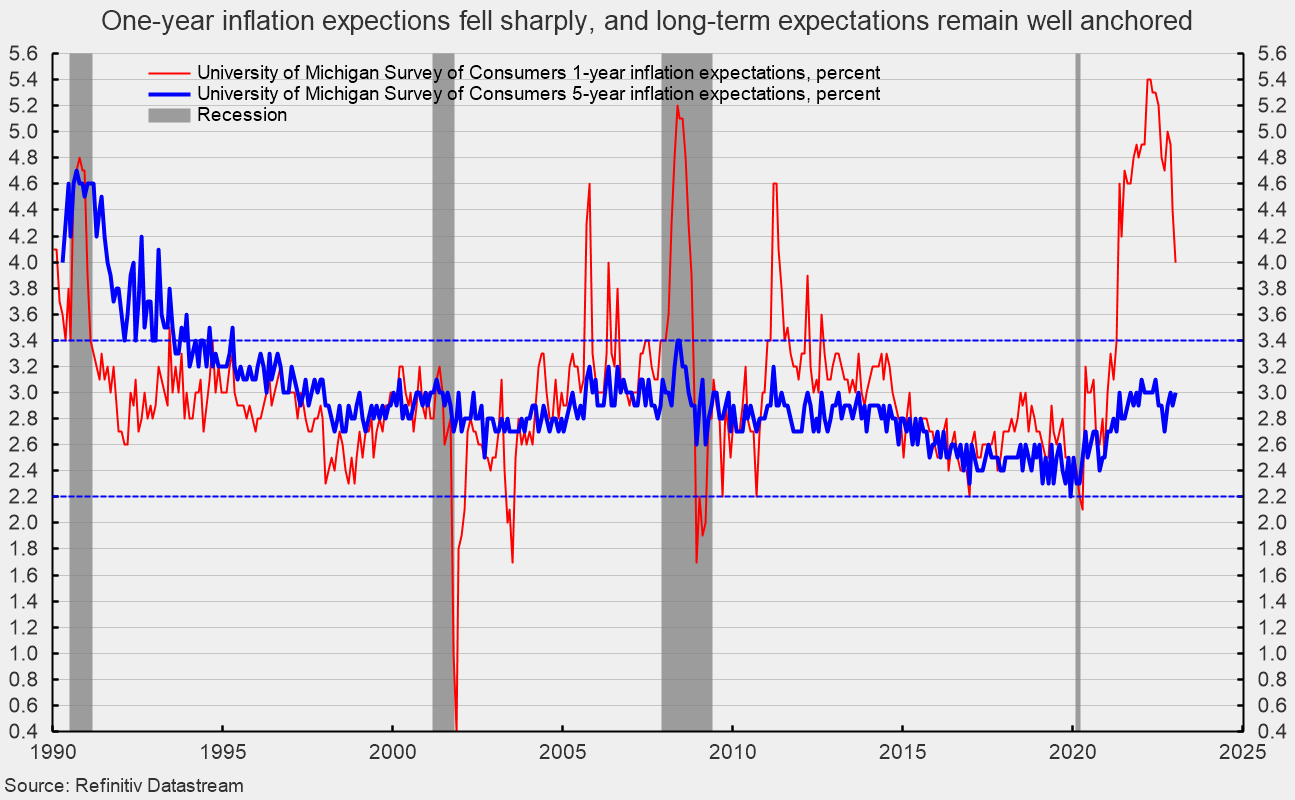

The one-year inflation expectations fell gain in January, declining for the seventh time in nine months to 4.0 percent. The result is significantly below the back-to-back readings of 5.4 percent in March and April, and the lowest level since April 2021 (see second chart).

The five-year inflation expectations ticked up in January, coming in at 3.0 percent. That result is well within the 25-year range of 2.2 percent to 3.4 percent (see second chart). The report notes, “Uncertainty over both inflation expectations measures remains high, and changes in global factors in the months ahead may generate a reversal in recent improvements.”

The overall levels of consumer sentiment measures remain low by historical comparison. However, significant improvements in recent months are a very positive sign. Despite those improvements, economic risks remain elevated due to the lingering impact of inflation, an aggressive Fed tightening cycle, and the continued fallout from the Russian invasion of Ukraine. The economic outlook remains highly uncertain. Caution is warranted.

THIS ARTICLE ORIGINALLY POSTED HERE.

– David Skarica")