The Fed has just published the newest edition of its Financial Stability Report. It covers what the most powerful central bank in the world perceives as risks to the financial system stability. Is it time for the gold bulls to uncork champagne?

Financial Sectors Appears Resilient, But…

The Fed’s assessment of the financial vulnerabilities in the latest Financial Stability Report has little changed since November 2018 when the report was inaugurated. The financial sector appears resilient, with low leverage and limited funding risk. It seems that gold will have to wait longer for a crisis that could push its prices out of the comfort zone.

However, there might be a glimmer of light at the end of the tunnel. The report point out two red warning signs. First, asset price valuations. Although some pressures have eased a bit since the latest report in November 2018, asset price valuations “remain elevated in a number of markets, with investors continuing to exhibit high appetite for risk.”

Indeed, equity prices relative to forecast earnings remain above the median value over the past 30 years. Similarly, real estate prices are high relative to rents. And spreads on leveraged loans have widened recently to level above the historical median, which reflects high demand for leveraged loans.

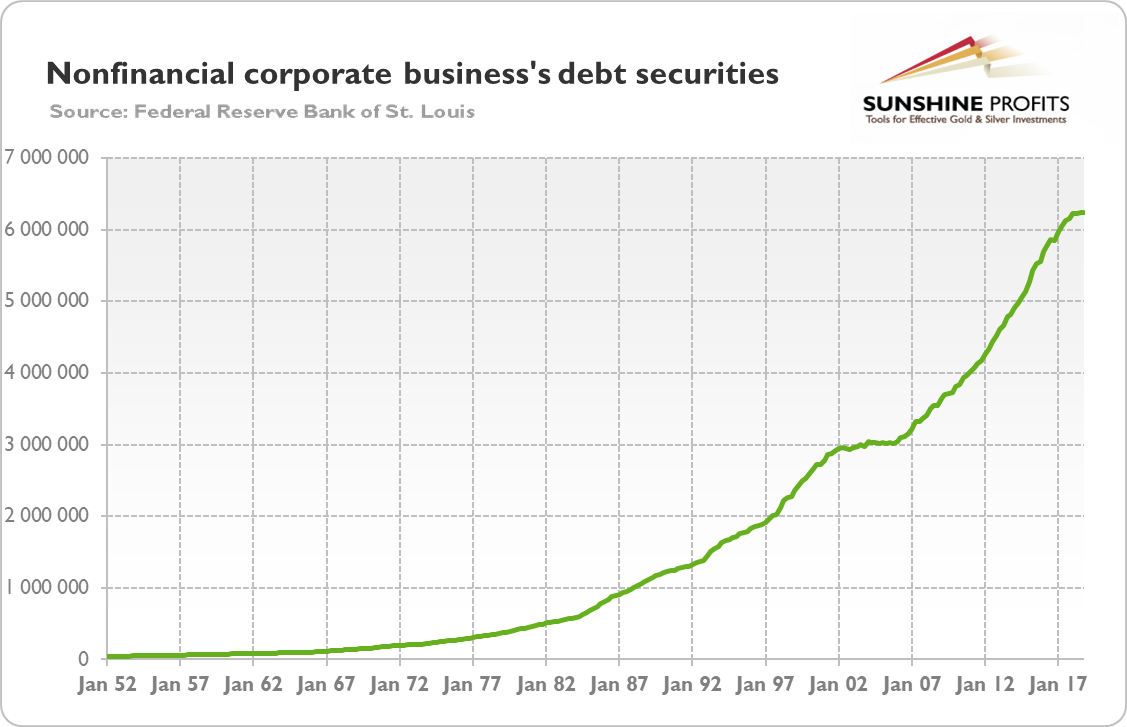

This is related to the second biggest threat for the financial stability noted by the Fed – the debt. As the chart below shows, the corporate debt has been on the rise.

Chart 1: Nonfinancial corporate business; debt securities; liability; millions of dollars, quarterly, not seasonally adjusted, from Q1 1952 to Q3 2018.

The problem is that, although household borrowing remains at a modest level relative to incomes, leverage in the business sector is high by historical standards, while the credit standards for some business loans have deteriorated further.

borrowing by businesses is historically high relative to gross domestic product (GDP), with the most rapid increases in debt concentrated among the riskiest firms amid signs of deteriorating credit standards.

What a surprise! Who would havethought that ZIRP may encourage excessive indebtedness? Or that low interest rates may draw in marginal borrowers and the most riskiest firms that would not get credit at higher rates?

So far, thanks to the easy monetary policy, the corporate indebtedness has not been very problematic. However, even the Fed acknowledges that “the elevated level of debt could leave the business sector vulnerable to a downturn in economic activity or a tightening in financial conditions.”

Elementary, my dear Watson. This is actually why the Fed is a hostage to the Wall Street. The tightening in financial conditions could indeed prove very harmful. This is because the share of bonds rated at the lowest investment-grade level has reached near-record level as more than 50 percent of investment-grade bonds outstanding are rated triple-B (just above the junk status), amounting to about $1.9 trillion. Thus, a slowdown in the global economy or tighter financial conditions would trigger downgrades of these bonds to speculative-grade ratings, possibly cascading through the financial markets.

Implications for Gold

The Fed is ringing the alarm over the increase in leveraged loans and corporate debt. That’s a big risk. If it materializes, the gold prices should go up. However, ringing the alarm does not equal to the economic crisis on our doorstep. The leveraged loan buildup is not a simple replay of the last financial crisis. One important difference is that before the Great Recession, loans made out to highly indebted businesses were chiefly the preserve of banks, but now they are mainly funded by hedge funds and other non-bank lenders. The banking sector’s balance sheets are stronger now than they were before the liquidity crunch of 2008.

Hence, the financial sector seems to be resilient. But the key world here might be “seems”. When interest rates are low, and the Fed is always ready to accommodate the needs of financial sector, everything looks great. But it might be an illusion. We still bet that the current expansion may still last for quite a while longer and thus not provide tailwind for gold. As they say, hope for the best but prepare for the worst. We will keep monitoring closely the corporate debt and leveraged loans – join us and check the June edition of the Market Overview!

If you enjoyed the above analysis, we invite you to check out our other services. We provide detailed fundamental analyses of the gold market in our monthly Market Overview reports and we provide daily Gold & Silver Trading Alerts with clear buy and sell signals. If you’re not ready to subscribe yet and are not on our gold mailing list yet, we urge you to sign up. It’s free and if you don’t like it, you can easily unsubscribe. Sign up today!

Disclaimer: Please note that the aim of the above analysis is to discuss the likely long-term impact of the featured phenomenon on the price of gold and this analysis does not indicate (nor does it aim to do so) whether gold is likely to move higher or lower in the short- or medium term. In order to determine the latter, many additional factors need to be considered (i.e. sentiment, chart patterns, cycles, indicators, ratios, self-similar patterns and more) and we are taking them into account (and discussing the short- and medium-term outlook) in our trading alerts.

Thank you.

Arkadiusz Sieron

Sunshine Profits’ Gold News Monitor and Market Overview Editor

THIS ARTICLE ORIGINALLY POSTED HERE.

– Stock Pick of the Month November 2024")

{kind=link}