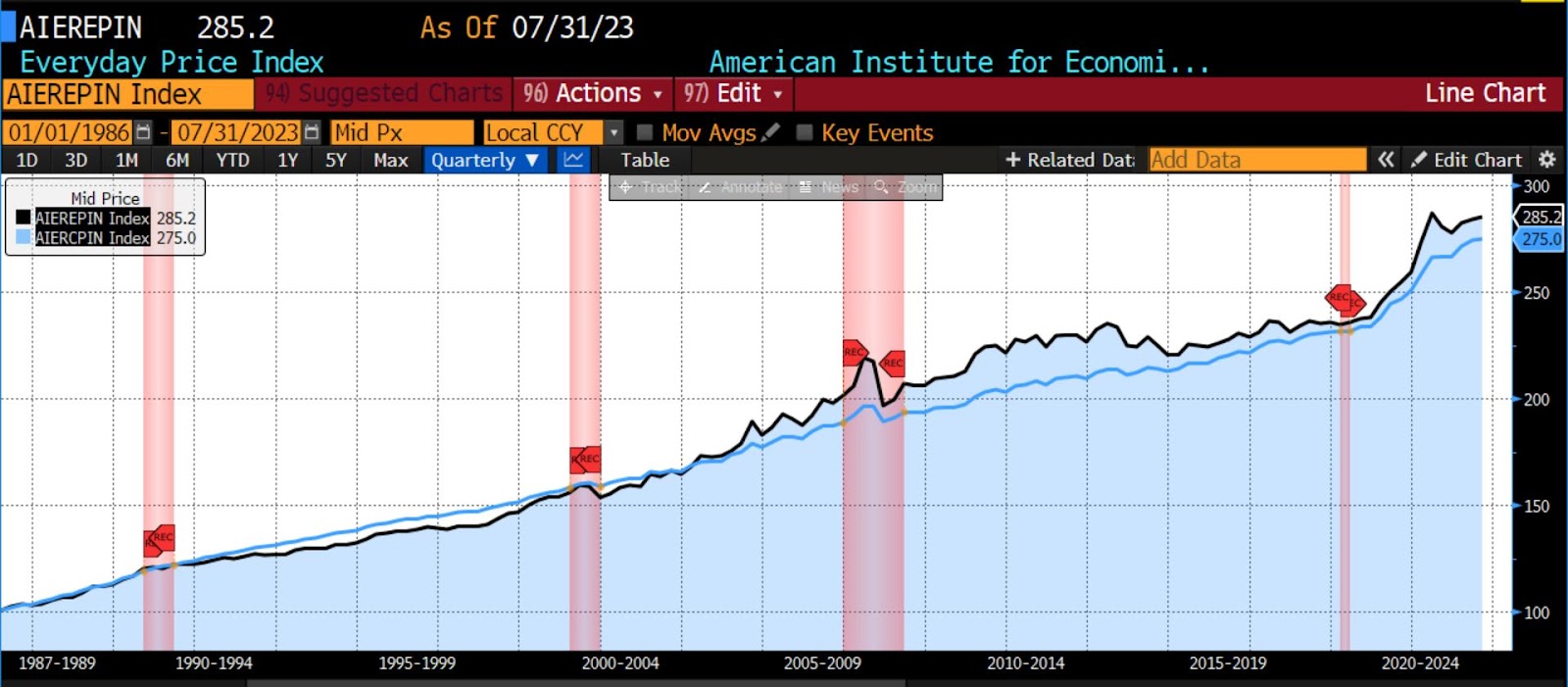

AIER’s Everyday Price Index (EPI) increased by 0.34 percent in July 2023. With this increase, the index stands at 285.2, 0.5 percent below its level one year ago in July 2022.

AIER Everyday Price Index vs. US Consumer Price Index (NSA, 1987 = 100)

(Source: Bloomberg Finance, LP)

The largest price gains among EPI constituents from June to July 2023 occurred in the food at home, food away from home, and housing fuel and utilities categories. The smallest declines in price were seen in recreational reading material, postage and delivery services, and audio discs, tapes, and other media. In three categories, no price changes occurred on a month-to-month basis in three groups: gardening and lawncare services, cable and satellite television and radio, and video discs and video disc rental prices.

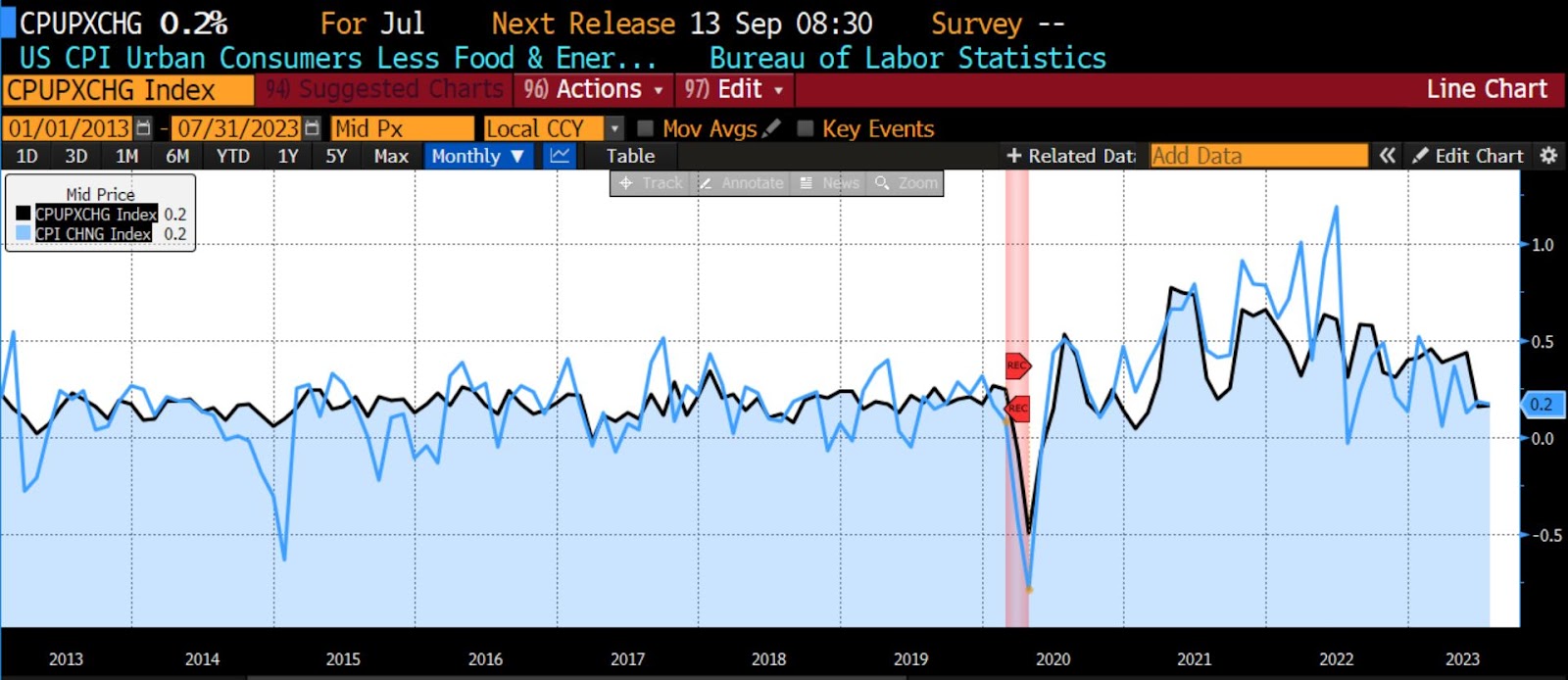

On August 10th, the US Bureau of Labor Statistics (BLS) released the July 2023 Consumer Price Index (CPI) data. Both headline CPI and core CPI (ex food and energy) rose by 0.2 percent on a month-over-month basis, which met expectations of 0.2 percent for each. Of note, the month-over-month change in core CPI represents the smallest increase in two years.

Ninety percent of the increase in the headline index was accounted for by increases in shelter costs, with additional contributions from motor vehicle insurance and food at home prices. The most sizable month-over-month decreases occurred in airline fares, used cars and trucks, and medical care.

July 2023 US CPI headline & core, month-over-month (2013 – present)

(Source: Bloomberg Finance, LP)

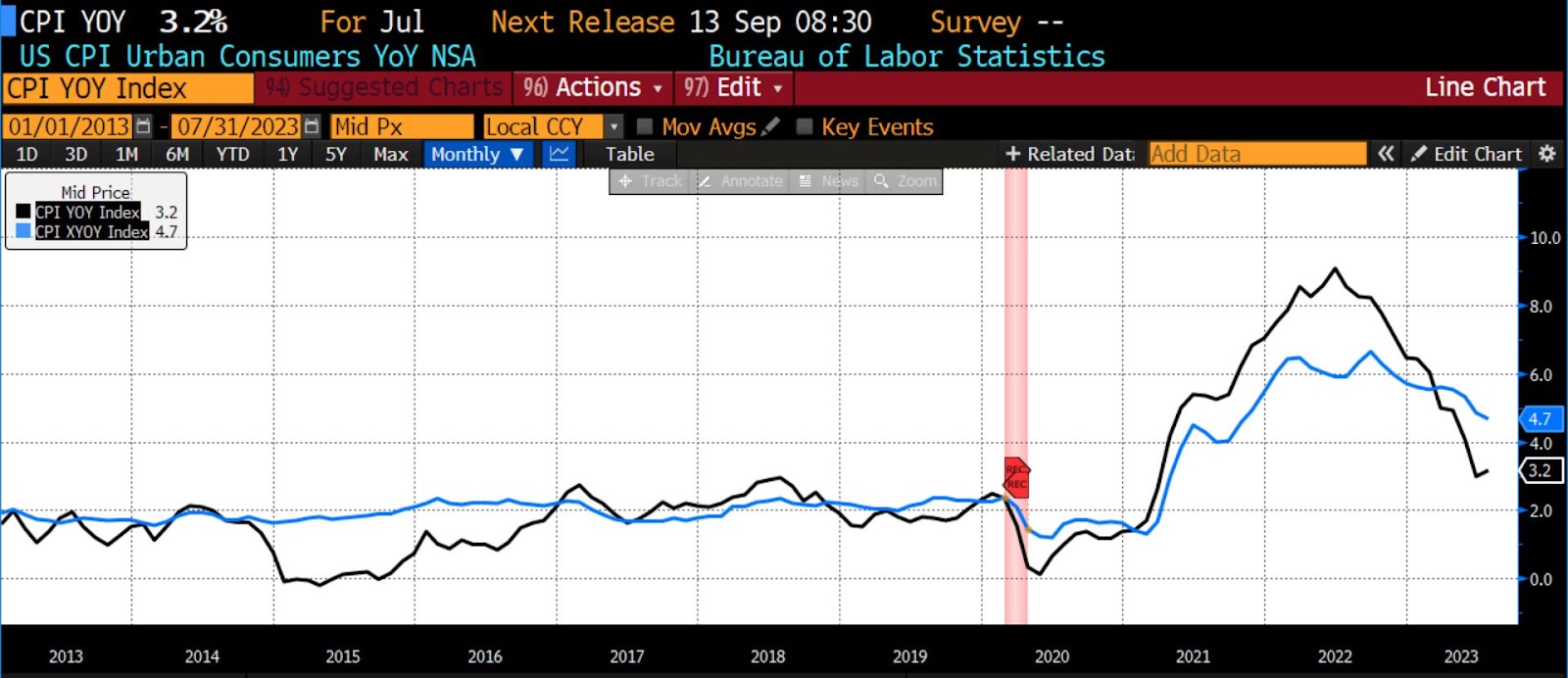

On a year-over-year basis, headline CPI rose 3.2 percent versus an expected 3.3 percent, while core CPI (ex food and energy) met expectations of a 4.7 percent rise.

July 2023 US CPI headline & core, year-over-year (2013 – present)

(Source: Bloomberg Finance, LP)

Core goods prices fell 0.3 percent in July 2023, which was the second straight month of decline. Additionally, both June and now July’s core CPI annualized on a one-month basis fell to 1.9 percent, indicating a slowing of momentum in price changes which meets the Fed’s 2 percent mandate. Higher-than-average temperatures throughout the United States over the past month have led to shorter operating hours for oil refineries which, up against vacation season demand, are sending gasoline prices higher. Thus both month-over-month and year-over-year headline numbers in the coming month or two may buck the disinflationary trend.

Policy rates are at their highest level in twenty-two years with speculation mounting regarding the number, size, and timing of additional rate hikes (if any) during the remainder of 2023. Credit conditions are tightening considerably at present as the money supply continues to contract for an eighth consecutive month. Additionally, the Fed’s most recent Senior Loan Officer Opinion Survey indicates not only higher risk aversion among lending executives but falling demand for credit as well. Recent softness in US labor markets, growing indications of slack in manufacturing, and consumer fatigue are the factors which the Fed will weigh against the continuing progress of disinflation going into the September 20th Federal Open Market Committee meeting.

THIS ARTICLE ORIGINALLY POSTED HERE.

– David Skarica")